Today, deposits are front and center of all banks’ business strategies. However, Simon-Kucher research and exchanges with industry players show that banks need to focus more on customer needs to unlock growth through deposit management. This article explores how taking a customer-centric approach can help banks tap into opportunities in the deposit landscape, and includes industry poll results from our recent webinar in collaboration with UK Finance.

Form placeholder. This will only show within the editor

Banks should provide a broader range of deposit products for customers

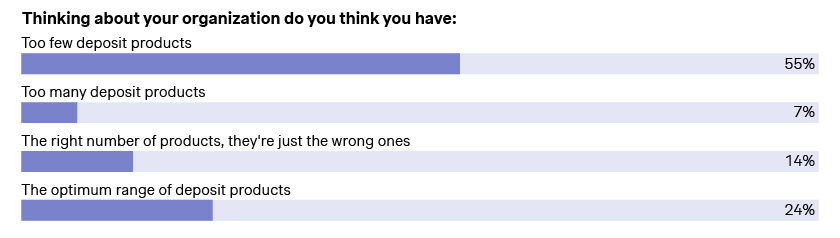

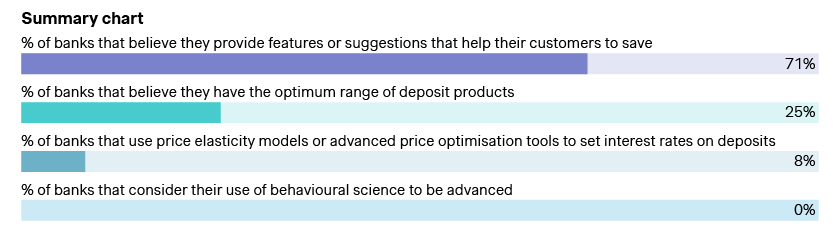

In our recent webinar with UK Finance, we asked members of the banking industry about how they viewed the range of products their organization offered to customers. Only 25% thought that they had the right product range, with over 50% suggesting they had too few products to meet customer needs.

We’d have to agree. Meeting the needs of more customers drives better growth.

Offering the right product range is not about having six as opposed to two products. It’s about understanding the customers you're targeting and having the right products to meet those needs. Some will care about rate, while others will be more concerned about access to the money or the ability to use the channel of their choice. By segmenting target customers and developing products and offerings to meet the needs of each segment, banks can ensure they have the right product range for their customer and business needs.

Fuel balance growth and manage interest expense through price optimization models

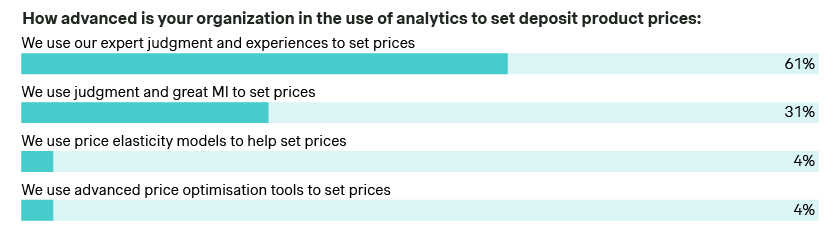

We also asked the webinar audience how advanced their organizations were in using analytics to set interest rates on deposit products. Over 60% stated they rely on nothing more than their own expert judgement and experience to set prices. Less than one in ten are using price elasticity models or analytical optimization tools.

Price analytics empowers banks to make data-driven decisions. Having developed analytics used to price over $1Bn of deposits, our experience at Simon-Kucher shows banks applying these models are able to harmonize portfolio growth with prudent interest rate management, ensuring the wellbeing of both customers and the balance sheet.

Incorporating behavioral science in banking

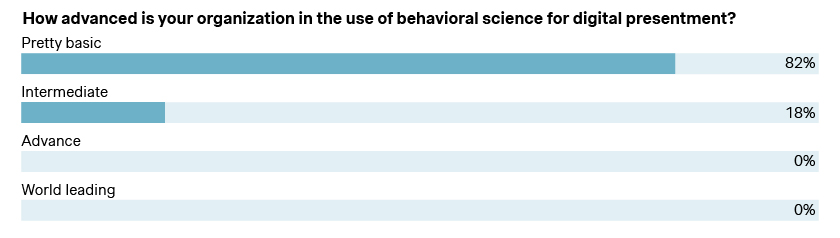

Another insight from our webinar with UK Finance was that banks should be more customer centric in terms of how they digitally present their products: Over 80% of our poll respondents considered their current use of behavioral science in this area to be “pretty basic.”

Banks can use behavioral science to better communicate their offers - particularly in a digital world where they have finely granular control over what’s presented to customers.

For example, working with one client, we put the exact same three offers to customers, but flipped the order in which they were presented. This simple change drove a 13% change in the relative take-up of the different offers.

We worked extensively with another bank to understand what messaging was important to their customers in the buying decision. In this instance, through careful research and pre-testing, we found that emphasizing risk avoidance was 50% more motivating in driving acceptance, click throughs, and ultimately product applications.

Don't just stop at product and pricing. Think about how to apply analytics and behavioral science to your well-crafted communication strategy. A simple change in presentation can drive better outcomes.

Banks need to do more to engage their customers

What factors truly matter to individuals when selecting a bank for their primary deposit account? Of course, things like opening bonuses and cashback offers are important, as well as the bank’s reputation and assurance that their money is insured. But there are two additional factors that stand out:

• Research conducted by Simon Kucher identified that almost a third of consumers expressed a strong preference for banks that offer features to make saving an engaging and enjoyable experience. There is a growing desire among customers for banking interactions that go beyond the transactional, emphasizing the importance of creating a dynamic and enjoyable savings journey.

• Secondly, almost a quarter of customers seek banks that actively assist them in achieving their savings goals. This signals the shift toward a more personalized, supportive banking relationship where customers value financial institutions that actively contribute to their financial wellbeing.

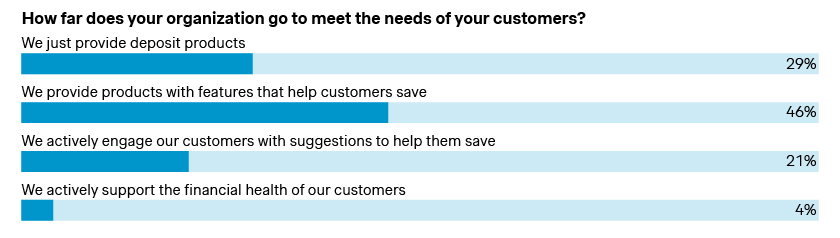

Here, the findings from our webinar poll are more positive, with over 70% of respondents stating that their organization did try to go beyond simply providing products to actively help customers save. However, only 4% felt that they actively helped support the overall financial health of customers, so there is still room for improvement.

Conclusion: Banks must go beyond just providing deposit products

A customer-centric experience is not just for the neobanks and fintech disruptors. Few banking products are sold face to face nowadays, and with the digital journey, everything can be constructed, improved, iterated on, and personalized.

However, as the results of our recent webinar polls show, banks need to focus on becoming more customer centric in order to fully tap into the opportunities and unlock better growth.

The good news is that in some areas the banks are already taking positive steps, particularly when it comes to actively helping customers to save. However, in other areas, particularly the use of behavioral science and price analytics there is still significant room for improvement.

It’s time to move closer to the customer, it’s time to get personal.