The 1950s – laying the groundwork

The semiconductor industry may seem like a modern marvel, but its origins in the 1950s tell a fascinating story of innovation, challenge, and economic transformation.

Introduction

The 1950s mark a foundational decade in the history of the semiconductor industry. Building on the transistor’s invention in the late 1940s, this period laid the groundwork for manufacturing capabilities and rudimentary pricing frameworks that would define the path of the rapidly evolving sector. During these formative years, semiconductor products were expensive novelties with very specific niches. They were primarily used in military applications and high-end research projects rather than mass consumer markets. Demand was modest but growing, driven by the potential of these new devices to replace bulky vacuum tubes and usher in more compact, efficient electronic systems.

This first article in our decade-by-decade series explores how the fundamental cost drivers of the 1950s shaped pricing decisions, influenced broader market strategies, and paved the way for what would later become one of the world’s most transformative industries. By understanding the opportunities, constraints, and economic conditions of this period, we see how strategic decisions around pricing models formed the bedrock of semiconductor commerce.

The dawn of semiconductor manufacturing

Semiconductors were born out of intense research efforts to find alternatives to vacuum tubes in switching and amplification circuits. The invention of the transistor at Bell Labs in 1947 provided an impetus for developing early manufacturing processes in the early 1950s. While the theoretical concepts for semiconductors were well-understood within research circles, large-scale fabrication was a major challenge. Silicon’s potential was known, but germanium-based transistors initially dominated because germanium was easier to work with at lower temperatures.

Cost drivers in early production

Hand Assembly: Early transistor production was extremely labor-intensive, leading to high unit costs. Much of the transistor assembly (mounting active junctions, attaching leads) and packaging the final device was done by skilled technicians using manual tools and microscopes. This constrained volume and inflated prices.

Low Yields: Process inconsistencies (impure materials, doping challenges, mechanical handling) meant a large fraction of transistors failed testing, so the cost of each successful device had to absorb the expense of the rejects.

Small Batches: Because demand was relatively low and yields were unpredictable, manufacturers produced semiconductors in small batches. Cost per device was often dictated by how many survived1 the fabrication process, which made pricing somewhat volatile.

Equipment and Materials: Specialized equipment—much of it adapted from other fields such as glass-blowing and vacuum sealing—was expensive and scarce. Meanwhile, semiconductor-grade materials faced similar supply limitations, further driving up costs.

Research & Development (R&D) overhead: in the 1950s, manufacturers were essentially learning on the job, refining processes with every batch. These R&D costs were often rolled into overhead, further raising per-transistor cost.

Cost element | Typical share of cost23 | Cost items |

|---|---|---|

Materials | 20–30% | Included germanium (or early silicon) wafer/slug, alloy dots or point contacts, lead frames, and the metal or plastic package. |

Direct Labor | 30–50% | Reflects substantial manual labor: each transistor could take 15–30 minutes for delicate assembly and rework. |

Overhead & Indirect Costs | 20–40% | Low yields (often <10–20%) meant many devices were discarded during testing, raising the effective cost of each functioning transistor. Overhead also included the expense of specialized equipment, plus ongoing process R&D |

Table 1: For a typical mid-1950s transistor retailing at around $10 (nominal 1950s dollars), direct manufacturing costs (materials + direct labor + overhead) might run $6–$8, leaving a margin to cover distribution, marketing, and profit. Actual proportions varied by company and year.

Major industry events of the 1950s and their impact on pricing

Government-funded research

Driven by Cold War imperatives, the U.S. government poured millions4 into semiconductor R&D. The U.S. Department of Defense (DoD) provided funding for research and development, prioritizing performance and reliability over cost. Bell Labs and other institutions rapidly advanced transistor technology, enabling better yields and gradually bringing down manufacturing costs. With military applications at the forefront, producers had incentives to streamline processes, but defense spending largely shielded them from severe price pressure. Essentially, government funding allowed manufacturers to recoup large portions of their R&D investments, mitigating the need for aggressive cost-based pricing. To illustrate just how important the U.S. government was during these early days, in the 50s ~80-90% of semiconductor capacity was absorbed by the U.S. DoD – today, as consumer applications have taken over that figure is ~4%.

Entry of early innovators

Companies such as Texas Instruments and Fairchild Semiconductor entered the market in the late 1950s. Their approach to production and emphasis on research into silicon-based transistors helped reduce dependency on germanium, potentially lowering material costs once silicon processing was refined. This gradual shift introduced a measure of competition, modestly influencing pricing strategies by the decade’s end.

Transition from Germanium to Silicon

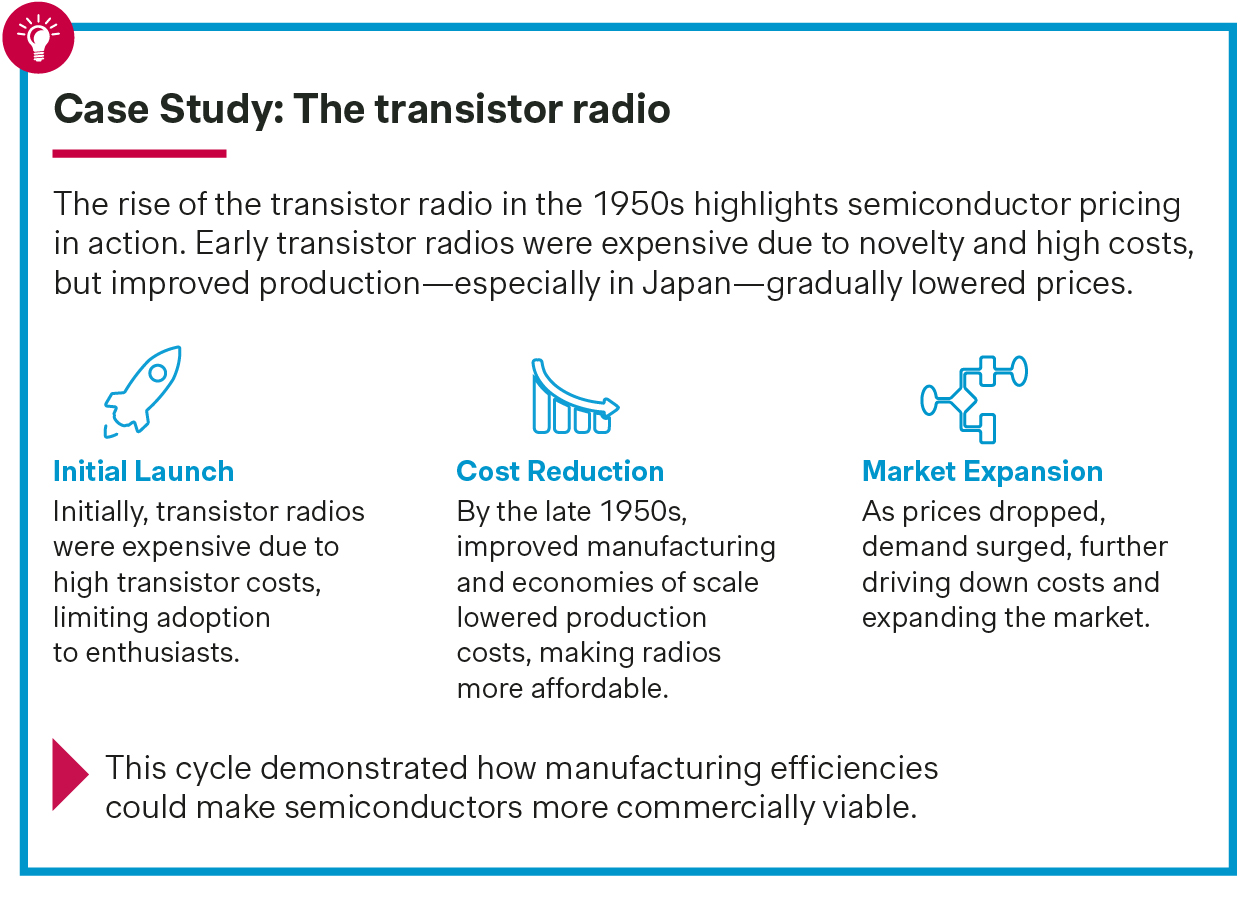

Though germanium was the initial workhorse, it had significant limitations, particularly regarding high-temperature performance. Silicon offered a wider operating temperature range and lower leakage current, which translated to more reliable devices. However, the switch to silicon required new equipment and manufacturing know-how—an upfront investment that temporarily sustained higher product prices. Despite these costs, silicon transistors eventually dominated, setting the stage for more cost-effective manufacturing in subsequent decades.Timeline of key pricing milestones in the 1950s

![chart 1]()

Manufacturing Costs and their influence on pricing

By the late 1950s, manufacturers were fully aware that improving yields could drive more aggressive pricing. Each step in the process—material purification, wafer slicing, device fabrication, and packaging—had its own inefficiencies. While the labor-centric model of production limited the speed at which costs could drop, incremental process refinements made a difference over time:

Material purity

With each improvement in crystal growth and doping techniques, the reliability of individual transistors increased, raising the effective yield. Cost-per-working-device therefore inched downward. This was instrumental in allowing for slightly lower end-user prices.

Packaging innovations

Packaging emerged as a crucial factor. Initially, transistors were encased in glass or metal cans. Better design and automation in packaging reduced defect rates. This not only cut production costs but also made transistors more robust, further fueling market demand.

Scale and learning curves

The concept of an experience curve—where costs fall as manufacturing volumes rise—was practically observable, though not formally studied in detail until later. Each batch run taught engineers how to refine temperatures, doping levels, and other parameters, gradually boosting yields.

Early pricing models

Three main pricing models emerged during the 1950s:

Premium pricing for novelty: The first transistors were priced high because they offered capabilities that vacuum tubes could not match. This premium was justified by lower power consumption, reliability, and form factor advantages. Defense and specialized research clients, who needed cutting-edge technology at almost any cost, were prepared to pay for it.

Bundled contract deals: For government and major commercial orders, semiconductor manufacturers often offered batch pricing or tiered discounts. This approach balanced manufacturers’ need for stable revenue streams against the procurement agencies’ push for cost containment.

Cost-plus in government contracts: Certain supply agreements with defense agencies were structured on a cost-plus basis, meaning the price was determined by actual manufacturing costs plus a fixed margin. While this model ensured profitability, it limited manufacturers’ incentives to drive down costs quickly—at least for the government portion of their business.

In hindsight, these early pricing structures directly reflected the small-scale, specialized nature of the nascent semiconductor sector. Without the broader commercial push that would come later, prices remained elevated, albeit slowly trending downward as volumes increased.

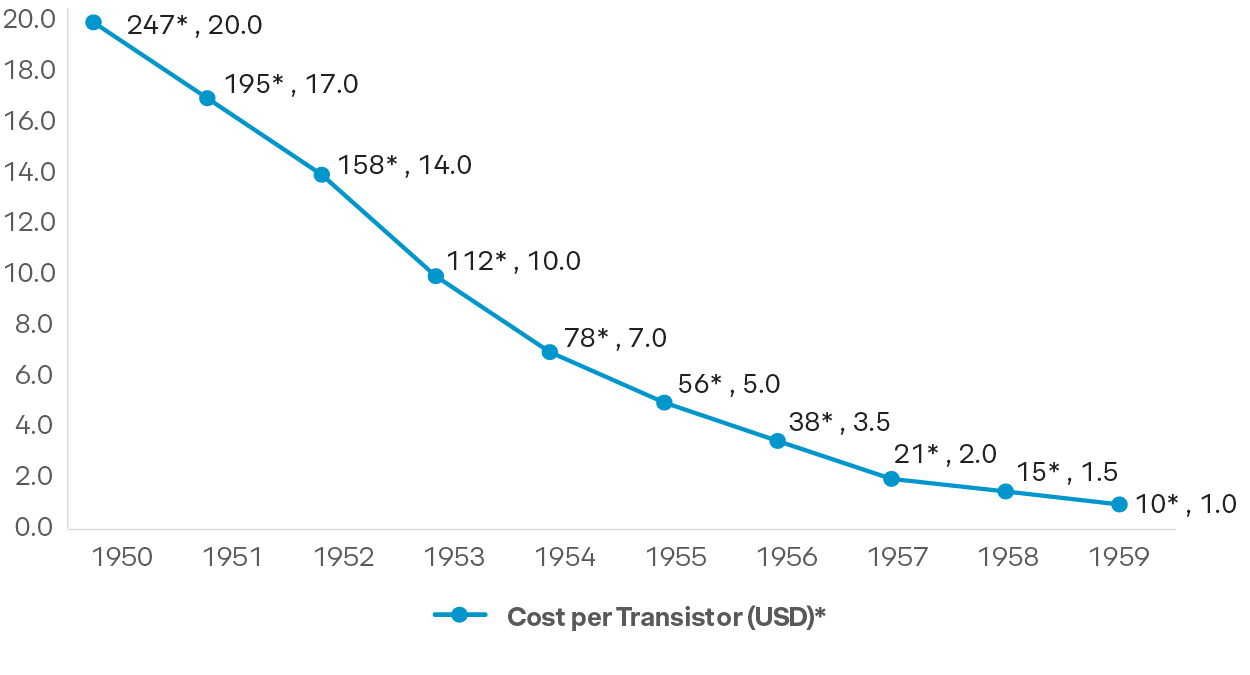

Approximate Cost Trend of a Single Transistor (1950–1959)

Figure 1: Approximate cost per single transistor 1950-1959; Approximate historical overview of cost per single (discrete) transistor from 1950 through 1959, based on data compiled from multiple historical and peer-reviewed sources. Because transistor manufacturing was still in its infancy through most of the 1950s, data on exact prices vary widely; the figures below should be interpreted as representative estimates. *2023 Inflation adjusted cost derived from BLS data (1950-2023).

Conclusion: The 1950s – the foundations of an Industry

The 1950s laid the essential framework for semiconductor pricing strategies that would evolve in later decades. Dominated by small-scale manufacturing, labor-intensive processes, and dependence on government funding, the industry was still in its infancy. The high cost of semiconductors reflected both their scarcity and their strategic importance to defense and specialized electronic systems.

Yet, even in this early period, we observe the seeds of future developments: the shift to silicon as the favored material, the reliance on yield improvements to reduce costs, and the gradual emergence of private sector demand through products like transistor radios. In the context of pricing, the critical driver was the relationship between yield enhancement and manufacturing scale. The tiny leaps in process refinement paved the way for slightly lower unit costs and expanded the pool of end-user applications.

Key Lessons

The decade underscores that price reduction in semiconductors has always hinged on both technological innovation and manufacturing refinement. Even in the 1950s, we see that modest scale increases and improved yields can unlock new markets by making the product more affordable. While the industry was still learning how to mass-produce at acceptable defect levels, the foundational strategies of cost management—materials research, process automation, and yield optimization—were already set in motion.

In future decades, these early lessons would be magnified many times over. As we progress into the 1960s in our next article, the introduction of the integrated circuit and further improvements in scale will radically shift the pricing conversation, paving the way for an industry that would transform modern technology and global markets.

The 1960s – The decade of integration

Recap

The 1950s marked the birth of the semiconductor industry, with transistors emerging as high-cost, niche products primarily used in military and research applications. Early manufacturing was highly manual, with low yields and high costs keeping production volumes small. Pricing was largely dictated by the need to recoup R&D expenses, and government funding—particularly from the U.S. defense sector—played a crucial role in sustaining the industry. By the decade’s end, companies like Texas Instruments and Fairchild Semiconductor had entered the market, and the shift from germanium to silicon had begun, setting the stage for future innovation.

Introduction

The 1960s were a pivotal decade in the semiconductor industry, characterized by major technological leaps that brought transistors out of their standalone packaging and into integrated circuits (ICs). Building on the groundwork laid in the 1950s, when transistors were expensive, niche components, the 1960s saw the semiconductor world begin to harness the advantages of scaling and integration. This rapid evolution not only expanded the market for semiconductor devices but also ushered in new pricing strategies, cost structures, and competitive dynamics.

At the heart of these changes was the transition from discrete transistors toward IC-based designs that combined multiple transistors and components on a single piece of silicon. The implications for pricing were far-reaching: manufacturers needed to adjust their cost models to account for higher yields, new production complexities, and rising demand from emerging applications such as computers, communications, and aerospace. By exploring this decade in detail—from the initial experiments in integrated circuits to the moment they became commercial mainstays—we gain valuable insights into how semiconductor pricing began to follow the famous curve of consistent cost declines that would define future decades.

The defining shift of the 1960s was the movement from separate transistors, diodes, and passive components toward combining these into a single, monolithic integrated circuit. Although the idea of integrating multiple components on a single substrate had been discussed in the late 1950s, it was in the 1960s that these concepts reached commercial viability.

Key contributions to the widespread adoption of the integrated circuit

Jack Kilby and Robert Noyce Drive Innovation

Jack Kilby of Texas Instruments and Robert Noyce of Fairchild Semiconductor are often credited with leading the effort that made integrated circuits a reality. Kilby’s 1958 demonstration of a working integrated circuit, followed closely by Noyce’s contributions to planar technology, showed that miniaturizing an entire circuit on a silicon wafer was more than a theoretical exercise.

Planar Process Innovation

Noyce’s planar process, developed at Fairchild, was revolutionary because it allowed semiconductor manufacturers to produce more reliable ICs at scale. It introduced photolithography to define circuit features, significantly improving yields. This planar approach remained at the heart of semiconductor manufacturing for decades, fundamentally influencing cost and pricing strategies.

Initial Skepticism, Then Rapid Adoption

In the early 1960s, integrated circuits were far more expensive per unit than discrete transistors, partly because yields were low and the manufacturing process was still maturing. Many companies initially questioned whether incorporating multiple components on a single chip made economic sense. However, as research continued, ICs began to showcase higher reliability, smaller form factors, and eventually cost advantages—factors that would dominate price discussions by the decade’s end.

Key Market Drivers of the 1960s

Military and Aerospace Demand

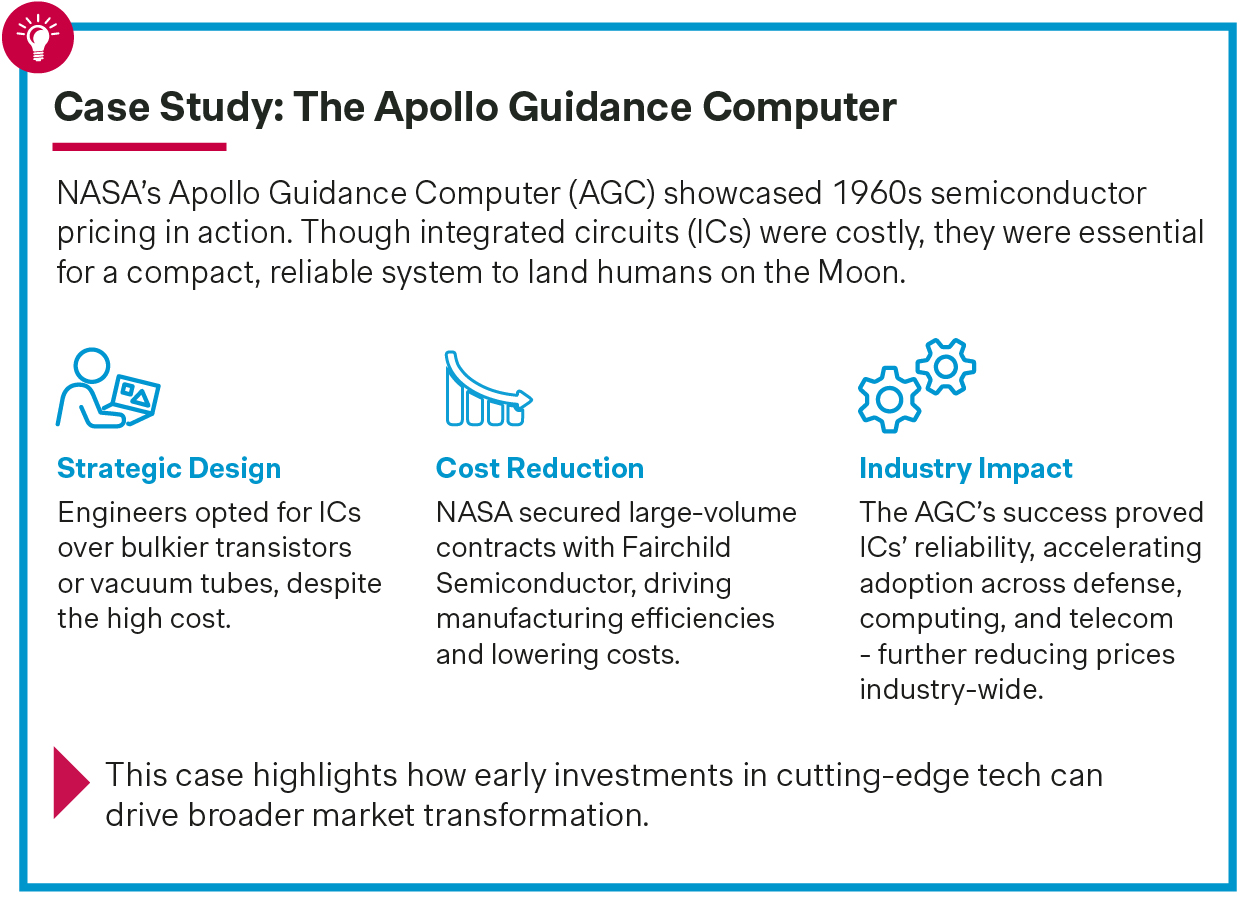

Like the 1950s, military and aerospace applications drove early volumes for integrated circuits. Programs such as the Apollo space missions demanded ultra-reliable, lightweight, and power-efficient components. NASA’s emphasis on advanced electronics spurred government contracts that could absorb the high costs of early ICs, helping manufacturers refine their processes without facing immediate cost pressures.

Mainframe Computers

IBM and other computer manufacturers began adopting integrated circuits for certain logic and memory functions. Although vacuum tubes and discrete transistors still played a role in larger systems, the 1960s marked the first notable shift toward IC-based modules in computers, particularly for specialized functions where reliability and density were paramount.

Telecommunications and Consumer Electronics

While consumer adoption of integrated circuits lagged the aerospace and computer markets, telecommunications infrastructure started incorporating ICs for switching and signal processing. By the latter half of the decade, smaller consumer electronics—such as advanced radios and early calculator prototypes—began experimenting with IC solutions. These consumer devices foreshadowed the explosion in mass-market demand that would characterize the 1970s and beyond.

Major Industry Events of the 1960s and Their Impact on Pricing

Formation of New Semiconductor Companies

The 1960s saw the birth of several key semiconductor firms—many founded by engineers from the so-called “Traitorous Eight” who left Shockley Semiconductor Laboratory to establish Fairchild Semiconductor. Spin-offs from Fairchild, in turn, led to the formation of companies like Intel (1968). This proliferation of new players fostered competition, innovation, and, eventually, more aggressive pricing strategies as multiple businesses sought to carve out market niches.

Transition from Bipolar to MOS Technologies

While bipolar transistors (used in TTL, or Transistor–Transistor Logic) continued to dominate the early integrated circuit market, metal-oxide-semiconductor (MOS) technology was quietly gaining momentum. MOS offered higher transistor densities and the promise of lower power consumption, though yields initially remained challenging. As some firms invested in MOS, they looked to differentiate themselves via higher integration levels—gradually influencing industry-wide conversations around cost reduction and volume-based pricing.

Government and NASA Partnerships

Like the 1950s, government contracts—particularly from NASA and various defense agencies—played a significant role. These organizations often operated on cost-plus contract structures, which ensured that semiconductor manufacturers could recoup their R&D expenditures. The difference in the 1960s was scale: ICs were becoming increasingly important in high-profile missions, such as Apollo, generating a more substantial revenue stream that helped companies refine processes and, over time, reduce costs.

Rise of the “Price-to-Performance” Paradigm

By the mid-1960s, forward-looking industry observers recognized a pattern: every new generation of integrated circuits packed more transistors into the same or smaller die area. This observation, later encapsulated in Moore’s Law (published by Gordon Moore in 1965), suggested that the number of components on a chip could double roughly every one to two years. Although Moore’s Law was initially intended as an observation rather than a pricing doctrine, it shifted the industry mentality from cost-plus approaches to an emphasis on improving cost-per-transistor.

Timeline of Critical Pricing Milestones in the 1960s

By the close of the 1960s, although discrete transistors still represented a significant slice of the semiconductor market, integrated circuits were on the cusp of becoming mainstream. Their price trajectory began to slope downward at a faster rate than discrete transistors had in the previous decade, powered by the synergy of government-backed R&D, competition among new entrants, and the compelling value proposition of functional integration.

Notable pricing models: shift toward value-based and volume-based approaches

With integrated circuits offering both increased functionality and better reliability, semiconductor companies in the 1960s began experimenting with new pricing models.

Value-Based Pricing

Because ICs could replace a collection of discrete components, some suppliers priced them based on their overall system value rather than a simple cost-plus margin. For military or aerospace buyers, the ability to reduce size, weight, and power consumption (SWaP) could justify a premium over traditional discrete solutions. This approach generated higher margins but depended on convincing buyers of ICs’ superior total value.

Volume-Based Discounts

As commercial interest in integrated circuits expanded—especially among computer and telecommunications equipment manufacturers—semiconductor firms began offering volume-based discounts. These arrangements incentivized large customers to commit to bigger orders, in turn giving manufacturers the economies of scale needed to drive down unit costs.

Contract Tiers and “Project Partnerships”

In some cases, semiconductor companies entered partnerships with large computer or aerospace firms. The semiconductor supplier would custom design an IC for a specific application in return for guaranteed purchase volumes. While costly to develop, these partnerships ensured stable revenue and accelerated learning curves—both factors that indirectly pressured pricing downward by improving production efficiency.

By the decade’s end, these emerging models collectively signaled that pricing strategies would no longer hinge solely on direct cost-plus formulas. Instead, the perceived value of integration—measured in performance, reliability, and reduced system complexity—became an increasingly important factor.

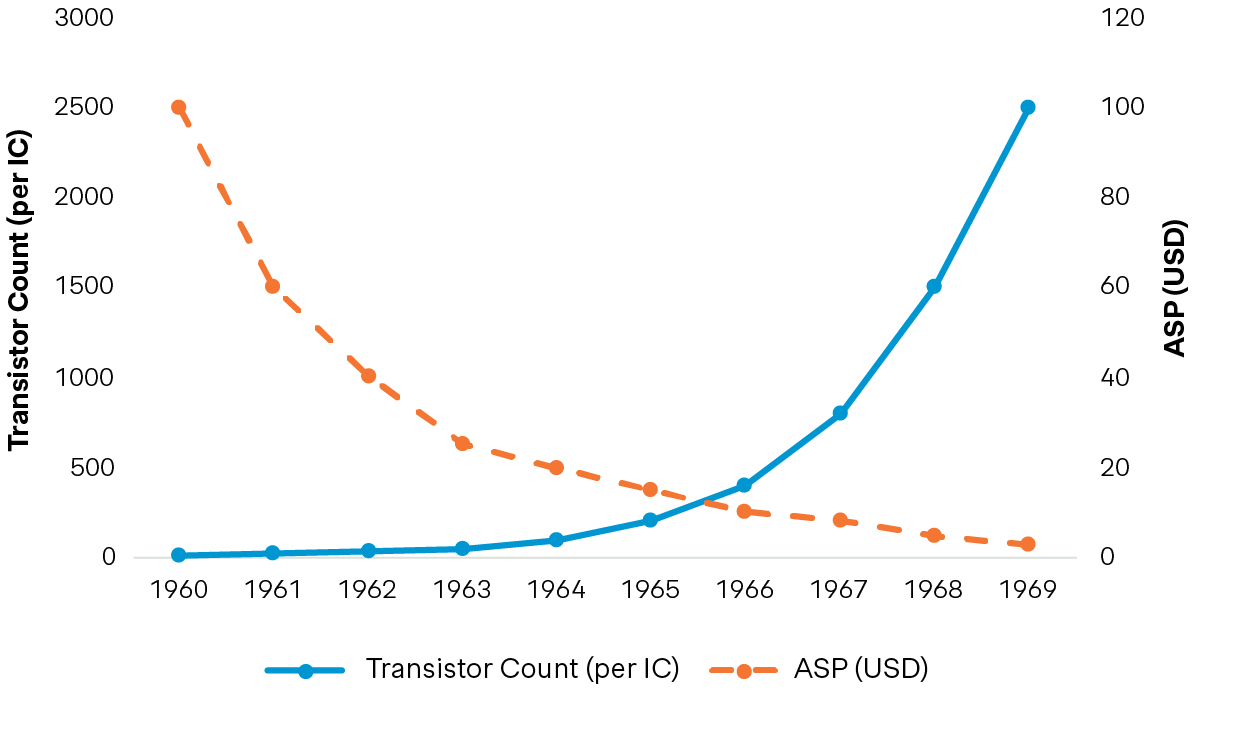

Transistor Count vs. Average Selling Price per IC (1960–1969)

This chart illustrates the fundamental dynamic that would become “Moore’s Law”: transistor density rose at an exponential rate, while simultaneous manufacturing refinements and economies of scale drove average selling prices down.

Figure 1: Figures are representative mid-range estimates. Actual data varied by manufacturer and data type. The transistor count reflects an average or typical small-scale integration device, such as a basic Transistor-Transistor Logic (TTL) or Diode-Transistor Logic (DTL) logic IC. High-complexity chips could exceed these figures by the late 1960s. The ASP data captures what was reported in trade publications.

Conclusion: The 1960s – The inflection point toward modern semiconductor pricing

If the 1950s were the infancy of semiconductors—driven by discrete transistors and dominated by cost-plus defense contracts—then the 1960s represented the industry’s critical leap into adolescence. The integrated circuit transformed the conversation from “Is solid-state technology viable?” to “How can we exploit integration to deliver more functionality at lower cost?”

Key enablers of this shift included the planar process, advancements in photolithography, government funding for large-scale aerospace projects, and the introduction of new semiconductor entrants that fueled competition. Pricing structures began to revolve around value and volume rather than simple cost-plus formulas. As transistor counts soared—doubling or more every couple of years—the per-transistor cost started on a steep downward slope that would define semiconductor economics for decades.

Key Lessons

The 1960s taught the industry that integration is an essential catalyst for cost reduction and market expansion. Although integrated circuits initially commanded premium prices, their superior performance, reliability, and form factor quickly justified higher costs in critical applications—thereby fueling the investment needed to refine manufacturing processes. The result was a self-reinforcing cycle of technological innovation and market acceptance that steadily drove down prices.

This decade also underscores the importance of strategic government and corporate partnerships. By funding large R&D projects and committing to volume purchases, these partnerships gave semiconductor manufacturers the runway to mature IC technology. The lessons from the 1960s resonate today: in a market defined by exponential growth in functionality and performance, pricing power often follows those who invest early in next-generation manufacturing and secure stable demand to justify scaling up.

In our next article—focusing on the 1970s—we will see how the foundation laid in the 1960s enabled semiconductors to break into broader commercial and consumer markets, triggering even faster improvements in cost-per-transistor and revealing new competitive dynamics that still shape the industry today.

The 1970s – Semiconductors go mainstream

Recap

Building on the costly, government-backed semiconductor efforts of the 1950s, the 1960s saw the revolutionary introduction of integrated circuits (ICs), moving beyond discrete transistors to more complex, multi-component chips. The decade was defined by the transition to large-scale manufacturing, supported by advances like the planar process, which significantly improved yields. While early ICs remained expensive, pricing strategies evolved, introducing volume discounts and value-based models. Military and aerospace applications drove early adoption, but by the end of the 1960s, the commercial potential of semiconductors—particularly in computing and telecommunications—was becoming clear.

Introduction

In the 1970s, semiconductors shifted from a niche technology reserved for government and specialized computing applications into mainstream electronic components that began transforming daily life. Building on the success of integrated circuits in the 1960s, semiconductor manufacturers saw the commercial market expand dramatically, fueled by the rise of personal computing, advanced telecommunications, and growing consumer demand for electronic products.

With the new era came new pricing challenges. As manufacturing technologies improved and volumes soared, cost-per-transistor continued its steep decline—a trend that made semiconductors more accessible to a broader range of applications. Yet macroeconomic events, changing trade policies, and intensifying global competition shaped a more volatile market. This article explores how semiconductor pricing evolved amidst both the promise of rapid technological gains and the pressures of a changing global economy.

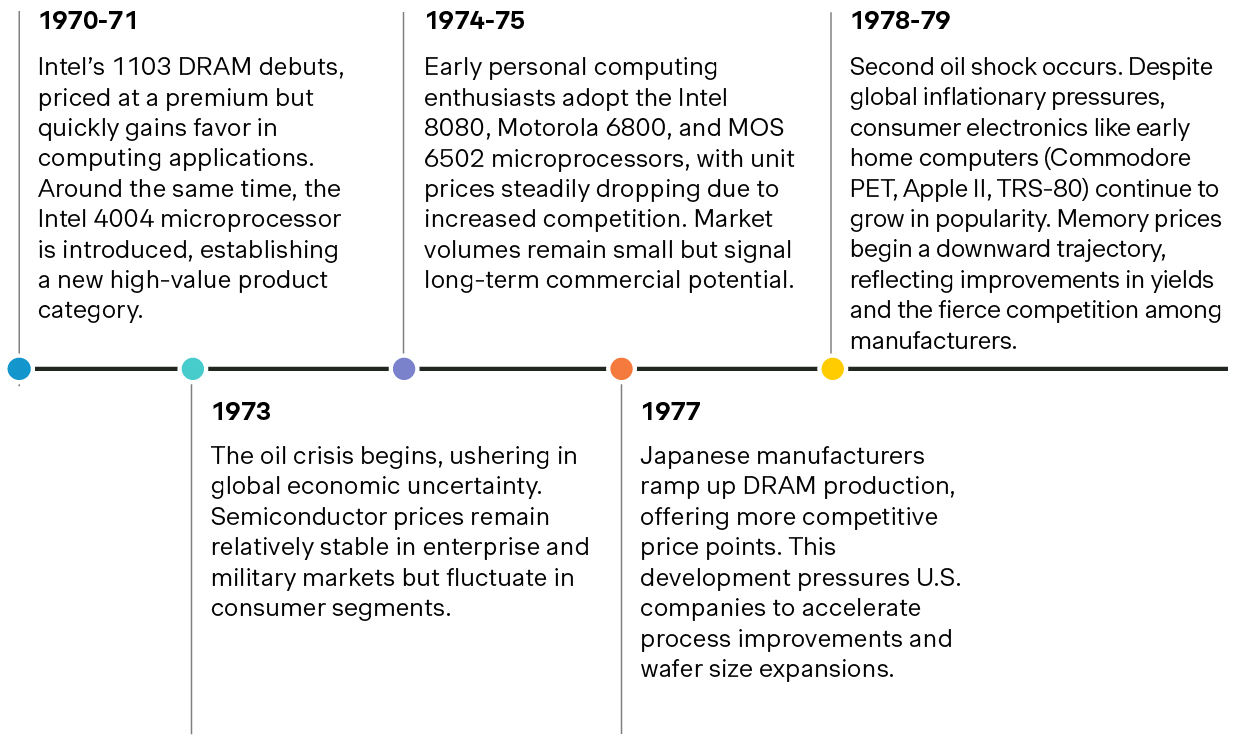

Global Market Expansion and Intensifying Competition

By the early 1970s, the semiconductor industry was no longer confined to a few pioneers in the United States. Japan began to emerge as a formidable player, particularly in the field of memory devices (Dynamic Random-Access Memory, or DRAM). Europe also fostered its own semiconductor ecosystem, with several companies investing in research and production. These global expansions fueled competition and price pressure as multiple regions vied for market share.

Japanese Producers

Firms like NEC, Hitachi, and Fujitsu focused on high-volume production of memory chips, undercutting many American counterparts on price. They quickly became known for strong process discipline and manufacturing efficiency, positioning themselves as serious contenders.

American Mainstays

U.S. companies—including Intel, Texas Instruments, Motorola, and Fairchild—responded to rising competition by ramping up R&D and expanding production capacity. Memory products such as Intel’s 1103 DRAM (introduced in 1970) gained traction in computing markets, spurring a race to develop higher-density, lower-cost memory devices.

European Firms

While trailing behind the U.S. and Japan in terms of scale, European semiconductor manufacturers (e.g., Siemens, Philips) collaborated with national governments to fund R&D projects. This public-private cooperation aimed to keep Europe in the technological race, though pricing in those markets was often higher due to smaller volumes and a focus on specialized products.

Amid intensifying global competition, semiconductor pricing strategies began incorporating sophisticated cost models that considered not just production expense but also currency fluctuations, tariffs, and regional trade policies. Though these factors would escalate further in the 1980s, they were already influencing the market in the 1970s, as cost advantages in one region could quickly erode if currency or trade conditions shifted.

Key Technological Advancements Shaping Pricing

The Microprocessor Revolution

One of the most significant introductions in the 1970s was the commercial microprocessor. Intel’s 4004, released in 1971, packed the core of a central processing unit (CPU) onto a single chip for the first time. This milestone opened the door to an entirely new category of devices—from calculators to industrial controllers to, eventually, personal computers.

Impact on Pricing: Early microprocessors were relatively expensive compared to simpler integrated circuits. However, they offered unprecedented value by consolidating complex logic functions into one piece of silicon. Manufacturers could command premium prices at first, but as competitors (e.g., Motorola with the 6800, MOS Technology with the 6502) entered the field, prices trended downward.

Memory Density Increases

Memory chips, particularly DRAM, saw major capacity jumps through the decade. In 1970, Intel’s 1103 DRAM offered 1 kilobit of storage; by the end of the decade, DRAM chips had grown to 16 or 64 kilobits. This exponential increase in density—mirroring Moore’s Law for logic devices—paved the way for cost-per-bit reduction.

Impact on Pricing: As bit density rose, the cost to manufacture each additional bit of memory plummeted, allowing a drastically lower cost structure. Companies that achieved reliable, high-yield production of larger capacity memory devices could offer competitive prices and still maintain healthy margins.

Process Node Shrinks

Although not as pronounced as in later decades, the 1970s continued the trend of shrinking process nodes (feature sizes). Smaller geometries allowed more transistors to fit on a die, leading to better performance and lower per-unit costs, assuming yields could be maintained. Photolithography techniques advanced, but they also raised capital expenditures for new fabrication equipment.

Impact on Pricing: Each successful node shrink typically allowed manufacturers to reduce the die size (and hence material costs) of a given design, but it required significant investment in updated fab technology. Companies with the resources to continuously upgrade their fabs gained a cost advantage, eventually reflecting in product pricing strategies that leveraged economies of scale.

Macroeconomic Factors: Booms, Busts, and Shifting Trade Policies

The Oil Crises

The 1973 oil crisis and the subsequent 1979 energy shock had global economic repercussions. When oil prices soared, inflation took hold, impacting both consumer demand and the cost structures of technology manufacturers. Electronics production did not slow as dramatically as some traditional sectors, but the uncertainty made pricing less predictable.

Impact on Pricing: On one hand, higher inflation and economic turbulence could dampen consumer appetite for discretionary electronics, threatening volumes. On the other, industries such as aerospace, industrial automation, and computing pressed forward, cushioned by government or enterprise budgets. This sector-level divergence affected how semiconductor makers balanced pricing for consumer vs. commercial or defense clients.

Currency Fluctuations and Trade Tensions

As the U.S. dollar’s strength shifted throughout the decade, American semiconductor firms sometimes faced profitability challenges in exports, especially as Japanese yen valuations and European currencies fluctuated. Furthermore, Japan’s industrial strategy promoted large investments in semiconductor capacity, an approach that resulted in surplus production at times—leading to price competition and, in some cases, allegations of dumping.

Impact on Pricing: Manufacturers had to account for exchange-rate risk in their pricing, sometimes hedging production or relocating assembly plants to regions with favorable trade conditions. This period foreshadowed more intense U.S.-Japan trade disputes over semiconductors in the 1980s, but the seeds of tension were already planted in the 1970s.

Timeline of Notable Pricing Milestones in the 1970s

Cost Structures: From Batch to (Semi-)Automated Lines

Throughout the 1970s, semiconductor fabrication became increasingly automated. Although still far from the levels of automation seen in modern fabs, significant reductions in manual handling contributed to better yields and lower costs.

Wafer Handling and Testing

Automated wafer-handling systems, introduced in the late 1960s, became more reliable in the 1970s. These systems reduced contamination—a critical factor in yield improvement. Meanwhile, automated testing equipment allowed for faster identification of defective dies.

Packaging and Assembly

New packaging designs (e.g., plastic dual in-line packages for integrated circuits) simplified assembly. While some aspects of wire bonding and die attachment remained manual, partial automation reduced labor costs and improved consistency.

Scaling Manufacturing Lines

To meet rising demand, manufacturers built larger fabs, often doubling or tripling capacity. This scaling created economies of scale—particularly as process yields improved—leading to a more pronounced drop in cost per device over time.

These improvements in manufacturing efficiency set the stage for more aggressive pricing. As volumes increased, some companies started to experiment with “learning curve” pricing, intentionally setting lower prices to capture market share, betting that higher volumes would reduce unit costs even further.

Notable Pricing Models in the 1970s

Premium Pricing for Emerging Products

Microprocessors, in their early years, commanded premium prices because they delivered high value to specialized applications. Likewise, cutting-edge DRAM chips with higher densities than competitors could initially fetch top dollar. Companies that were first to market with advanced chips enjoyed a temporary pricing advantage until rivals caught up.

Commodity Pricing for Established Products

As memory densities matured and multiple suppliers flooded the market, DRAM, SRAM, and certain logic families began to exhibit commodity-like price behaviors. Margins on these products narrowed as competition and volumes soared, leading to frequent price fluctuations based on supply-demand dynamics.

Contract Manufacturing and OEM Discounts

Major computer and telecommunications OEMs (Original Equipment Manufacturers) secured dedicated capacity and volume-based discounts. For instance, if a large computer firm signed a multi-year contract for a specific microprocessor or memory device, the semiconductor supplier could confidently invest in scaling production, thereby lowering costs and offering preferential pricing. This partnership approach gave both parties predictability in cost and supply.

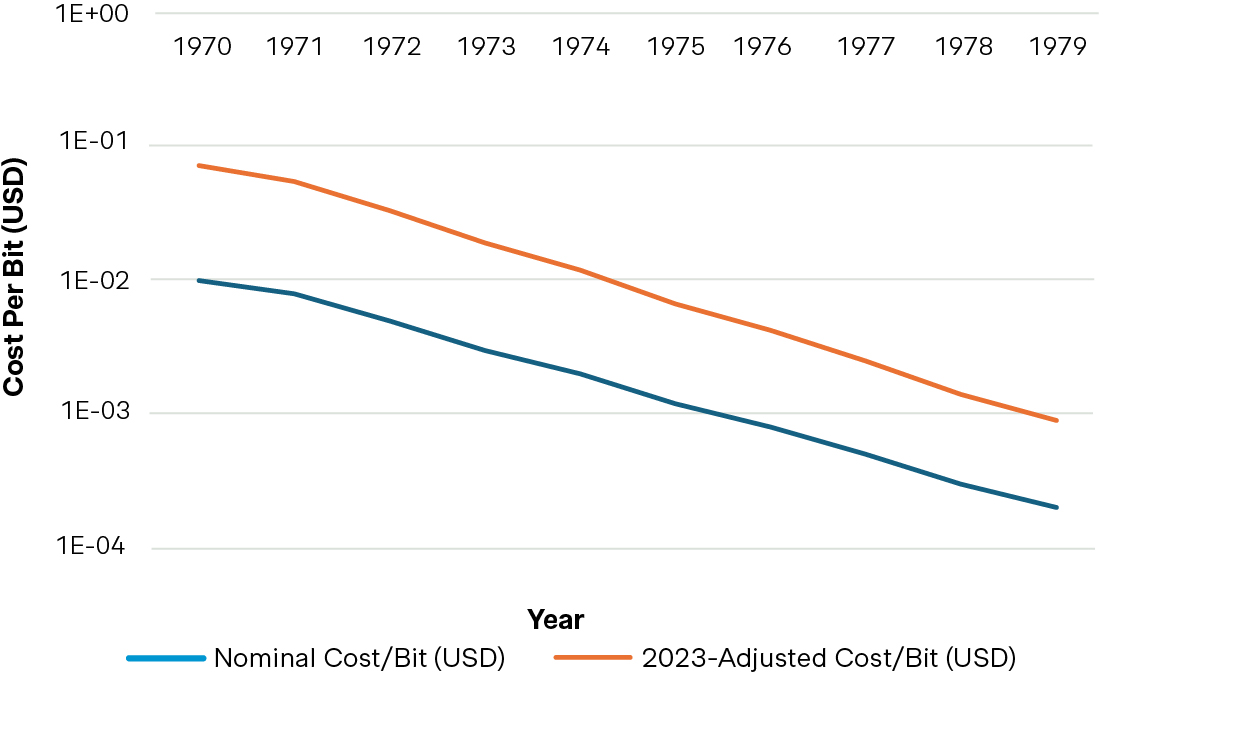

Cost per Bit of DRAM (1970–1979)

Figure 1: Different DRAM generations (1K vs. 4K vs. 6K) came to market at different times. The annual data here is a broad average for the "typical" product available in that year, not the newest or the cheapest. Actual contract or volume-discounted prices could deviate significantly from these 'List Prices'

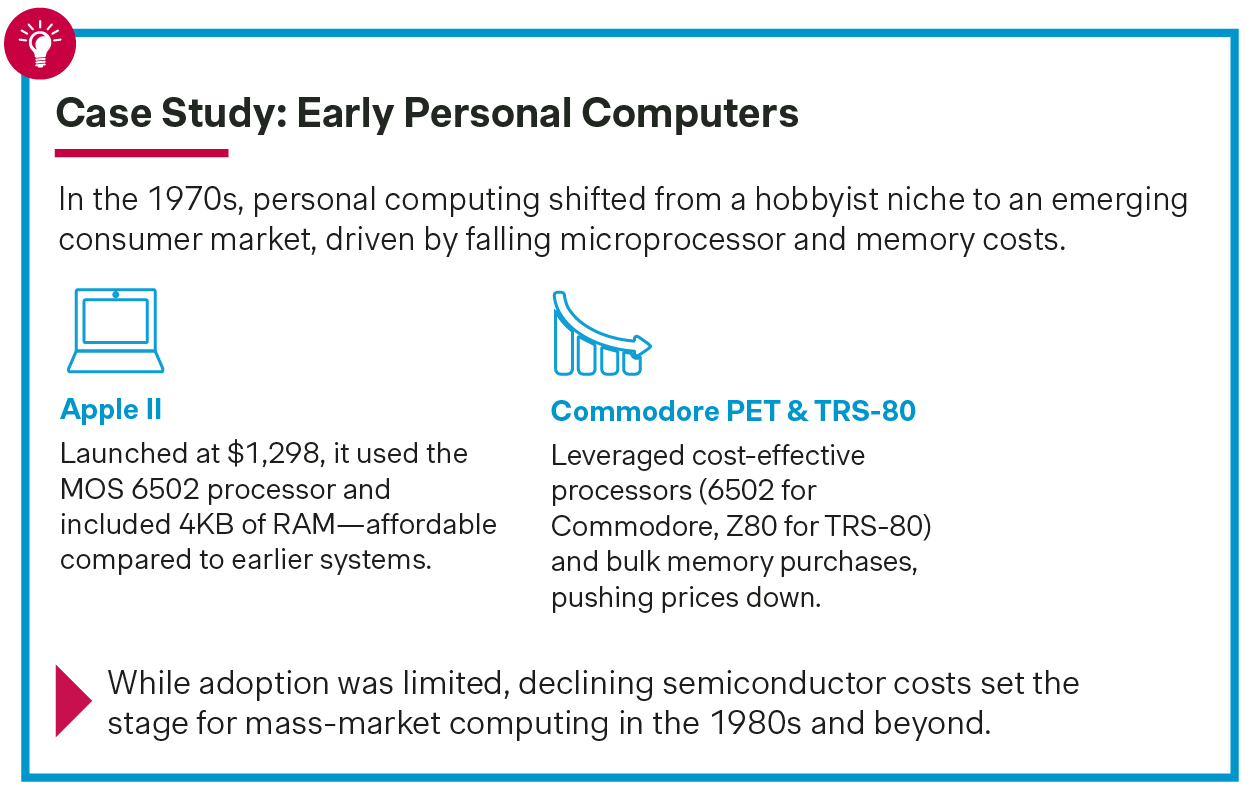

Case Study: Early Personal Computers

In the 1970s, personal computing shifted from a hobbyist niche to an emerging consumer market, driven by falling microprocessor and memory costs.

Apple II: Launched at $1,298, it used the MOS 6502 processor and included 4KB of RAM—affordable compared to earlier systems.

Commodore PET & TRS-80: Leveraged cost-effective processors (6502 for Commodore, Z80 for TRS-80) and bulk memory purchases, pushing prices down.

While adoption was limited, declining semiconductor costs set the stage for mass-market computing in the 1980s and beyond.

Conclusion: The 1970s—Bridging Pioneering Innovation with Widespread Adoption

The 1970s stand out as a dynamic period when semiconductors made the leap from specialized applications to mainstream electronics. Propelled by the microprocessor revolution, dramatic improvements in memory density, and broader automation in fabrication, the industry experienced sharp declines in cost-per-transistor. At the same time, macroeconomic upheavals like the oil crises and emerging trade competition—especially from Japan—introduced new uncertainties and pressures.

Pricing strategies evolved in step with these changes. While cutting-edge products such as microprocessors still commanded premium prices, many devices—especially memory chips—began to behave more like commodities. The interplay between technological leaps (yielding cost reductions) and intensifying global rivalry (forcing price competition) laid the foundation for the sophisticated pricing models that would define the next phase of semiconductor growth.

Key Lessons

The central takeaway from the 1970s is the power of market forces in driving semiconductors into everyday use. As R&D breakthroughs and large-scale manufacturing lowered costs, previously exclusive technologies found a place in consumer products like calculators, game consoles, and fledgling personal computers. However, this growth also highlighted vulnerabilities to macroeconomic shocks and shifting trade environments. For modern pricing strategists, the 1970s underline the importance of both scaling efficiently and diversifying markets—ensuring that demand is balanced across sectors that are not uniformly exposed to economic downturns.

In the next installment of this series, we will explore the 1980s—a decade marked by further technological refinements, the rise of new device categories, and increasingly competitive global trade dynamics that would forever reshape how semiconductor products were priced and marketed.

The 1980s – Global Expansion and the Rise of Strategic Pricing

Recap

Semiconductors transitioned from high-cost, government-funded projects in the 1950s to the mainstream adoption of integrated circuits in the 1960s. The 1970s accelerated this momentum, driven by the rise of personal computing, memory chips, and telecommunications. Global competition intensified as Japan emerged as a major player, challenging U.S. dominance in semiconductor manufacturing. Pricing became more complex due to macroeconomic events like inflation, trade policies, and energy crises. While manufacturing costs declined with better yields and economies of scale, the decade also saw early trade disputes and the beginning of semiconductor price wars.

Introduction

The 1980s formed a remarkable bridge between the foundational shifts of the 1970s and the explosive innovations of the 1990s. Semiconductors, once primarily the domain of large-scale computing and specialized industrial applications, were fast becoming ubiquitous components in personal computers, consumer electronics, telecommunications, and automotive systems. At the same time, global competition reached new heights, fueling both fierce price wars and major strides in process technology.

Pricing models in the 1980s grew more complex and strategic. Manufacturers grappled with surging demand but also faced significant volatility: trade friction (particularly between the United States and Japan) escalated, currency fluctuations made planning difficult, and production overcapacity at times led to steep price drops. Despite these challenges, the enduring trend of declining cost-per-transistor continued—yet this decade also demonstrated that technology leadership alone was not enough to guarantee profitability without astute pricing and market strategies.

In this fourth installment of our historical series, we examine how semiconductor pricing models evolved in response to new market dynamics, government interventions, and major technological milestones. Understanding this era illuminates many of the foundational practices that still influence modern-day semiconductor pricing and global supply chains.

Shaping Forces of the 1980s Semiconductor Market

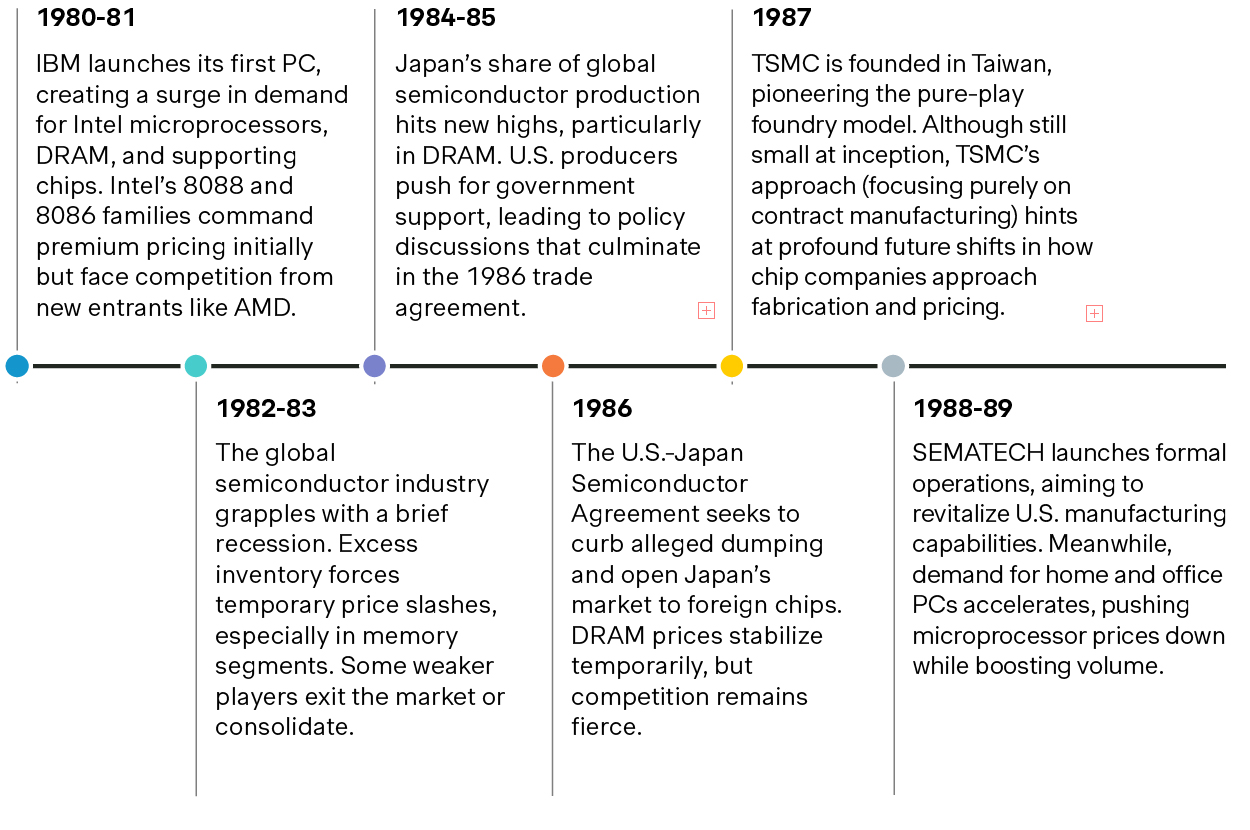

PC Revolution and Mass Adoption

By the early 1980s, personal computers were moving from a hobbyist curiosity to a household reality. Home and small-business computing boomed, largely thanks to IBM’s PC (introduced in 1981) and subsequent clones that adopted Intel’s x86 architecture. The rapid adoption of these machines had a profound impact on semiconductor demand, especially for microprocessors, memory chips, and supporting logic.

Microprocessor Leadership: Intel’s x86 family quickly became the dominant central processing unit (CPU) line for personal computers, creating massive demand for its microprocessors. A combination of volume-driven cost reduction and intellectual property licensing (to companies like AMD) helped shape pricing strategies that would remain relevant for decades.

Memory Bottlenecks: As software grew more sophisticated, PCs required increasingly larger amounts of DRAM. Combined with new generations of graphical user interface (GUI)-based operating systems, this translated into brisk volume growth—though not without price swings tied to global capacity expansions.

Growth of Telecommunications and Industrial Automation

Alongside the PC boom, telecommunications expanded with digital switching systems, satellite communications, and the beginnings of mobile telephony. These new markets demanded large volumes of reliable semiconductors for signal processing and network infrastructure. On the factory floor, programmable logic controllers and robotic systems further broadened industrial use cases. Demand was growing across multiple sectors simultaneously, intensifying competition among semiconductor producers.

Entry of Emerging Markets

While the U.S. and Japan dominated global production, other regions—particularly South Korea and Taiwan—began investing heavily in semiconductor manufacturing. Samsung in South Korea, for example, laid the groundwork for what would become one of the world’s leading memory and logic suppliers, while in Taiwan the founding of TSMC (Taiwan Semiconductor Manufacturing Company) in 1987 introduced the concept of a pure-play foundry model. Although these entrants were still ramping up in the 1980s, they foreshadowed a more geographically distributed industry.

Major Industry Events and Their Pricing Repercussions

U.S.-Japan Trade Tensions

During the mid-1980s, the United States accused Japanese semiconductor companies of dumping memory products (particularly DRAM) at below-cost prices in the U.S. market. American producers struggled to compete on cost and, in some cases, found themselves pushed out of high-volume segments.

Impact on Pricing: Following negotiations, the two countries signed the 1986 U.S.-Japan Semiconductor Agreement, which aimed to address dumping concerns and open up Japan’s market to foreign semiconductors. In practice, it led to some stabilization of prices in certain memory segments, but it also highlighted the increasingly political nature of semiconductor pricing.

Formation of SEMATECH

Concerned about the competitiveness of the U.S. semiconductor industry, key players and the U.S. government joined forces to form SEMATECH (Semiconductor Manufacturing Technology) in 1987. The consortium facilitated collaborative research among U.S. semiconductor companies to improve manufacturing processes and reduce costs.

Impact on Pricing: By sharing best practices and pooling resources, SEMATECH aimed to accelerate yield improvements and technology adoption, indirectly influencing pricing by helping U.S. firms remain cost-competitive with Japanese memory producers.

Shifting Wafer Sizes and Process Advances

Throughout the 1980s, wafer sizes increased from four inches to six inches (and some early adoption of eight-inch wafers by the very end of the decade). Process geometries shrank from the several-micron range into the sub-micron realm, laying the groundwork for higher densities and faster device performance.

Impact on Pricing: Larger wafers and improved yields meant more chips per wafer, driving down per-unit manufacturing costs. However, capital investments for new fabs soared, and this higher financial risk made strategic pricing decisions critical to recover massive R&D and equipment expenses.

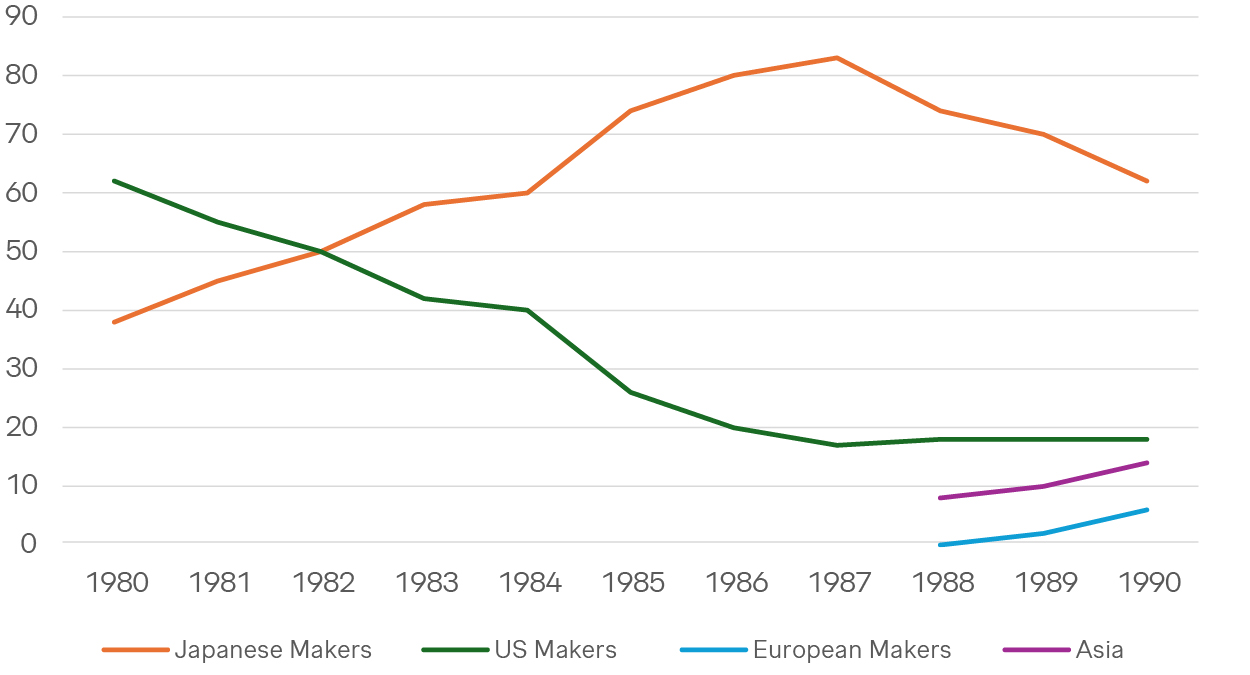

Global share of DRAM Sales manufacturing (1980-1989)

Timeline of Key Pricing Milestones in the 1980s

Evolving Cost Structures and Yield Imperatives

In many respects, the 1980s represented a coming of age for semiconductor manufacturing. While the industry had already embraced partial automation, this decade saw more advanced fab equipment, tighter process controls, and new packaging technologies.

Advanced Lithography

Steady improvements in photolithography equipment—such as the transition to deep ultraviolet (DUV) wavelengths—enabled sub-micron geometries by the decade’s close. Although each iteration demanded hefty investments, successful nodes provided a significant cost-per-transistor advantage.

Wafer Size and Throughput

Moving to larger wafers effectively multiplied the number of dies per run. Still, it required retooling or building new fabs with updated robotics, cleanroom standards, and high-precision wafer-handling systems. Once yields improved, the cost-per-chip advantage justified these investments.

Packaging Innovations

DIP (Dual In-line Package) remained common early in the decade, but more advanced packaging options—like plastic leaded chip carriers (PLCCs), pin grid arrays (PGAs), and surface-mount technology (SMT)—gained popularity. Although packaging was a smaller portion of total manufacturing cost than wafer fabrication, incremental changes in this area yielded minor but relevant cost savings.

All these refinements worked in tandem to lower the effective cost of producing semiconductor devices. Yet, they also increased the upfront capital burden, intensifying the imperative to balance prices, volumes, and market share to recoup massive fab investments.

Shifts in Pricing Models: From Cost-Plus to Strategic Differentiation

Value-Added Differentiation

With rising competition, many companies began differentiating their products through unique features—such as lower power consumption, on-chip cache memory for microprocessors, or specialized coprocessor functions. Instead of relying on a simple cost-plus margin, manufacturers increasingly priced their devices based on the specific performance and reliability advantages they delivered.

Intel and AMD

Intel initially commanded premium prices for x86 CPUs by offering new performance features and leveraging its ties with IBM and other major PC makers. AMD, legally licensed to manufacture x86 chips, often priced its versions more competitively to gain share, challenging Intel to refine both its technology and pricing strategies.

DRAM Suppliers

DRAM manufacturers sought to differentiate on reliability, speed grades, or packaging conveniences. Yet, as memory became more commoditized, many found they had to rely on operational excellence and scale to maintain margins.

Commodity vs. Specialty Markets

By the mid-1980s, segments of the semiconductor market had started to resemble commodity markets—particularly DRAM, where numerous suppliers produced similar products at large volumes. In these commodity-like arenas, price often became the deciding factor once a manufacturer had demonstrated baseline reliability.

By contrast, specialty applications—such as military-grade components or custom ASICs (Application-Specific Integrated Circuits)—remained less price-sensitive. Manufacturers serving these niches could afford to set higher margins, provided they delivered validated performance and long-term reliability.

Case Study: IBM's Adoption of Intel and the Rise of the Clone Market

IBM's choice of Intel x86 microprocessors for its original PC architecture sparked the rise of "clone" PCs. This decision made Intel and later AMD central to the PC revolution.

Market Impact: IBM legitimized Intel's x86, keeping prices strong initially. The clone market exploded after Compaq and others reverse-engineered the IBM BIOS, driving down prices and increasing demand for x86 chips.

Pricing Dynamics: Intel maintained premium pricing for its latest CPUs while lowering prices for older models. AMD offered cheaper alternatives, forcing Intel to improve performance at better value.

IBM’s CPU decision shaped industry pricing trends, establishing a lasting competitive dynamic between Intel and AMD.

Conclusion: The 1980s—Where Semiconductor Pricing Met Geopolitics and Scale

The 1980s took the semiconductor sector beyond the era of purely technology-driven cost declines and into a more complex reality. Demand surged as personal computers, telecommunications, and industrial automation expanded rapidly. Meanwhile, new producers—particularly in Asia—stepped onto the global stage, intensifying competition. Macroeconomic forces, from trade wars to national consortia, played critical roles in shaping how prices moved.

On the one hand, the continuous improvement in wafer sizes, lithography, and yield optimization maintained the long-standing tradition of declining cost-per-transistor. On the other hand, trade disputes and allegations of dumping highlighted how semiconductor pricing was no longer just about engineering breakthroughs but also about political and economic leverage. Companies that mastered both the technology roadmap and global market dynamics found themselves best positioned to thrive.

Key Lessons

The 1980s underscore the fact that semiconductor pricing cannot be decoupled from its broader environment. While Moore’s Law kept transistor costs on a downward trajectory, the actual end-user pricing hinged just as much on global capacity, macroeconomic trends, and government interventions. The period also reminds us that strategic product differentiation—delivering real value beyond raw technical specs—allowed certain segments (like microprocessors) to maintain healthier margins even in the face of mounting competition.

Looking ahead, the 1990s would bring another wave of transformation: the Internet’s emergence, the further rise of mobile communications, and the era of deep sub-micron manufacturing nodes. As we continue our journey through semiconductor history, these historical insights form the backdrop for understanding how today’s complex, globally networked industry came to be—and how pricing strategies might evolve next.